One critical and expensive phase of mortgage risk doesn’t show up in a servicing system.

It’s the quiet window between job loss and first contact, where:

- Savings drain faster than anyone expects.

- Confidence collapses.

- Anxiety shows up as avoidance, not returned calls.

- Families quietly wonder how their servicer can help.

During this phase, families go from job loss to long-term unemployment. While a forbearance can inject some opportunity, for too many who’ve been stuck in long-term unemployment, it can feel like an extension of hopelessness with an inevitable hard ending.

Let’s dive into the correlation between early intervention, mortgage success, and a topic often overlooked: the lived experience of long-term unemployment (LTU).

The Reality of Long-Term Unemployment

The risk in the quiet phase before delinquency isn’t theoretical:

- Over 20 million workers are laid off or separated each year

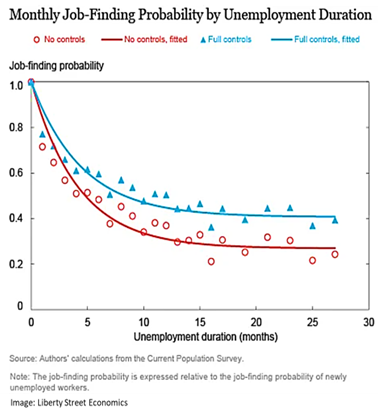

- The chances of landing a job drop substantially as unemployment weeks drag on

- Workers receive about half of their former wage – if they qualify for unemployment insurance

- 40% of all unemployment claimants run out of benefits, often at six months, before landing a job

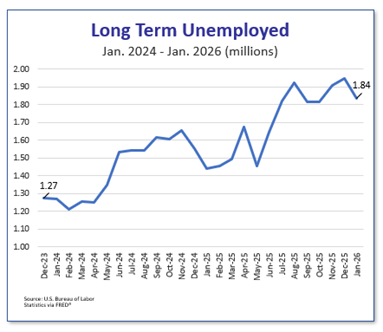

In the past two years, through January 2026, we’ve seen a troublesome cooling in the labor market:

- Unemployment rates climbed from 3.7% to 4.43%

- Long-term unemployment has grown 44%, up 560,000 to 1.8 million Americans stuck

- Time to land a job has risen from 20.8 to 24.4 weeks

This prolonged time being stuck has a psychological toll which directly undermines a borrower’s capacity to problem solve and engage and the longer someone is out of work, the harder it becomes to get rehired. Skills atrophy, networks go cold, and employers become hesitant about long gaps.

The Impact on Mortgage Defaults & Recidivism

As unemployment has grown, U.S. households have also taken a toll financially. Personal savings rates have dropped significantly. From Pandemic highs and, from baseline pre-pandemic November 2019 to November 2025, they’ve dropped from 6.9% to 3.5%. As savings erode, the ground beneath homeowners grows increasingly unstable, they don’t just tighten their belts on groceries and outings—they often struggle to make the mortgage payment on time, or at all.

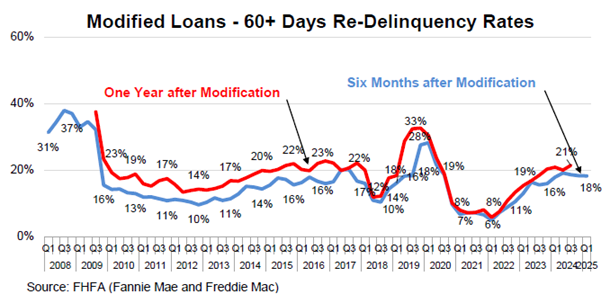

And part-time gig jobs that let a borrower pay part of their mortgage for a while can be perilous over time. Data shows that 18% of recently modified GSE loans fall 60+ days delinquent again within six months after modification, with redefault concentrated among borrowers with prior serious delinquency or weak income, especially in relationship to their debt.

What Can Be Done: a Reemployment Triage Model

Early intervention in reemployment is one of the most powerful levers servicers have to prevent a missed payment from becoming a foreclosure and a customer relationship from becoming a write off.

Early Signals - Servicers don’t have to wait for 30 day delinquency. Even more so with today’s AI-enhanced predictive models it’s possible to:

- Spot early stress signals in payment behavior and balances.

- Estimate which loans are most likely to become delinquent.

- Help distinguish unemployment driven risk from short term cash flow bumps.

This can open the door to a different approach: Not one program for everyone, but a triage system that matches support to risk and timing in three escalating steps.

1. Rising Risk, Before Delinquency: Online Tools & Teaching

- Use AI guided signals (payment shifts, reduced income) to start a calm, early conversation about job loss—perhaps six months before default.

- Offer self guided tools: job search checklists, resume help, networking tips, and short career literacy modules.

2. Elevated Risk: Webinars & Group Support

- For those with ongoing stress, add web workshops on job search best practices

- Include group participation, in a way that reduces isolation

3. Early Delinquency: One on One Expert Coaching

- For borrowers who become delinquent, offer individualized reemployment coaching and concentrate human support on households at the highest risk.

- Align coaching with loss mitigation so income recovery and loan workout support each other.

In a cooling economy with rising unemployment and shrinking savings, servicers have a growing opportunity to layer in employment focused triage alongside existing practices. By adding early education, group support, and targeted coaching to today’s toolkits, they can better manage emerging risk while helping more families stabilize and keep their homes.

To learn more about how servicers can proactively manage unemployment delinquencies, ask us about NextJob’s Homeowner Reemployment at info@nextjob.com.