By John Courtney, CEO, NextJob

October 9, 2025

The labor market is a mirror of our nation’s economic health—and the past month suggests the reflection is showing some troubling cracks in the labor market that the Federal Reserve’s rate cuts were designed to address. Below we look at the most recent data and trends over the past 24 months.We’ll learn more in the coming weeks and hopefully see a reversal.

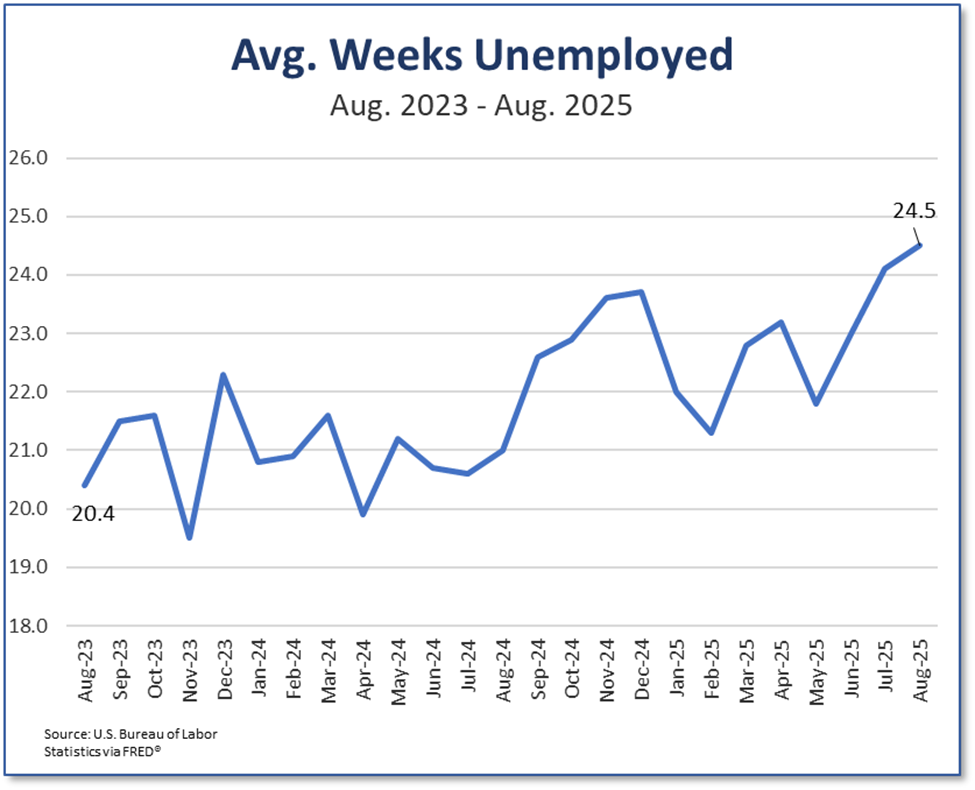

Duration of Unemployment - One Month Longer

While weekly unemployment claims improved recently (and were slightly lower in today’s report) after a large jump up in early September, the duration of unemployment has been climbing steadily over recent months. Over the past two years it has climbed nearly one full month from 20.2 to 24.3 weeks.

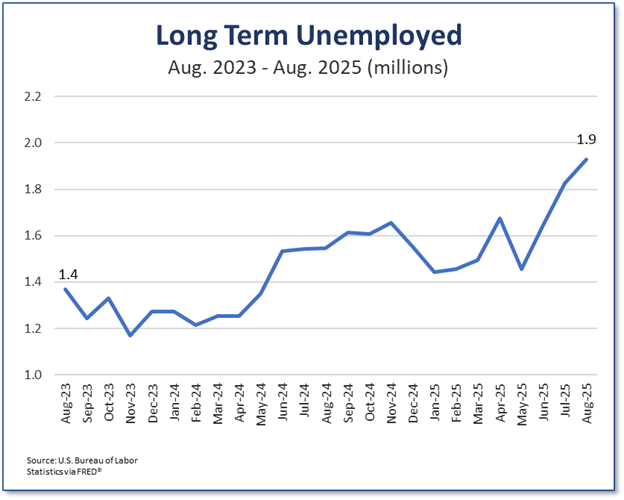

Long-Term Unemployment - Up 41%

Meanwhile the number of long-term unemployed—those out of work for 27 weeks or more—reached over 1.9 million in August 2025, a two-year climb of 41% from under 1.4 million in August 2023.

Job Growth - Slower

Job creation cooled as August 2025 saw a net gain of 22,000 jobs, compared to 79,000 jobs added in August 2024 and 215,000 in August 2023. Previous month downward revisions added further concern and, for September, ADP, LinkedIn and Indeed reports suggest a hiring slowdown.

Announced Layoffs and the Role of AI

While layoffs are not high, announced mass layoffs have grown, signaling potential future reductions in the workforce. Some may be due to artificial intelligence adoption accelerating, with the share of workers using AI rising from 20% to 40% in two years. According to a recent Goldman Sachs Research report, if AI technologies are widely adopted, 6-7% of U.S. jobs could be displaced, with entry-level and white-collar positions expected to be most affected.

Overall, these labor market and financial shifts mean more families see a job loss translate more quickly into missed payments and, often, deeper financial distress.

Financial Stress & Mortgage & Auto Loan Delinquencies

The job market has led to financial stress. As one homeowner said: “There were moments of self-doubt, questioning whether I was doing everything right or if I just wasn’t standing out in such a competitive job market. I knew I needed help, but I didn’t know where to turn or what resources were available to really make a difference.”

The numbers match:

- Savings - Limiting families’ buffers against hardship, the personal savings rates dropped from 5.3% in September 2023 to 4.6% two years later in August 2025, according to the Bureau of Economic Analysis’s report.

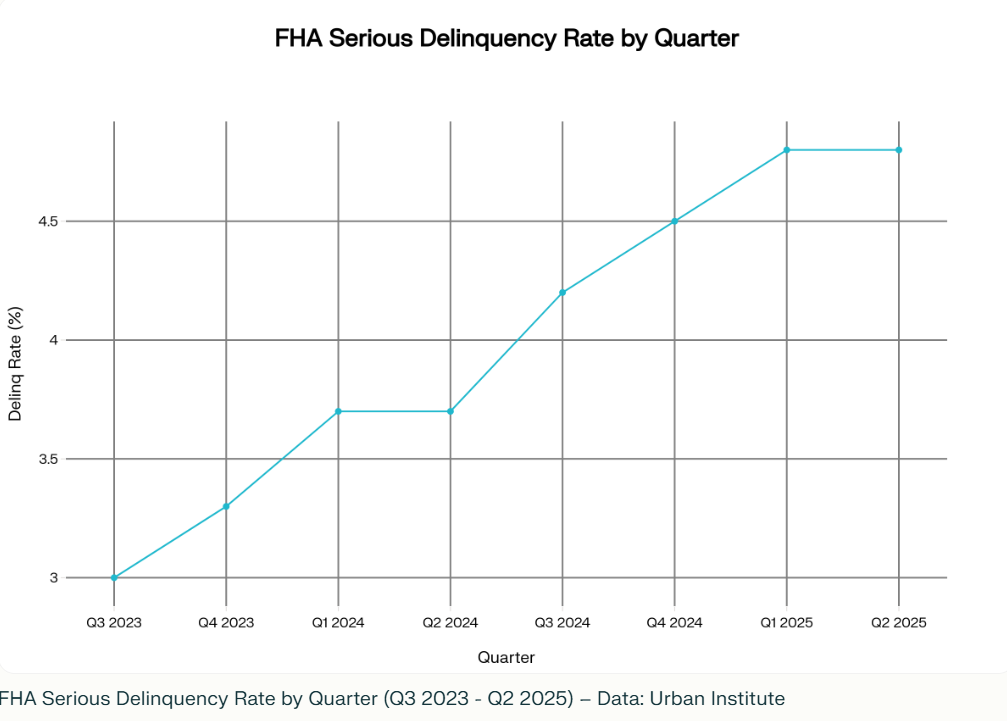

- FHA Delinquencies - According to HUD, the FHA mortgage delinquency rate increased over two years from 9.5% to 12% in Q2 of 2025, the highest rate since the pandemic. Meanwhile serious delinquencies rose from 3% to 4.8%. It appears recent policy changes may increase the rates further as policy changes aim to stem serial workouts.

- Auto Loans - U.S. auto loan serious delinquency rates also grew in the last two years--from 4.4% to 5.0%--with repossessions hitting post-2009 highs and defaults over 2.3 million—signaling risk levels not seen since the financial crisis according to recent reports from the New York Federal Reserve, LendingTree, and Axios.

The Value of Active Reemployment Support

Losing income can make it hard to keep a home, but there are ways forward. Homeowner reemployment has demonstrated proven results, helping borrowers land jobs, cure delinquencies and keep their home.

To learn more or join the movement, ask us about NextJob’s Homeowner Reemployment at info@nextjob.com.